APTT lodged its preliminary prospectus and is currently doing book building for its IPO.

My broker from DBS sent me the book building term sheet and here are the key terms.

Offering size - 1,393,696,000 units.

Cornerstone - 451,068,000 units. (about 31.4% of offering size)

Placement tranche - 917,628,000 units

Public offering - not less than 25m units.

Book building price range - $0.92 to $1.00 per unit

Distribution yield - FY2013 8.93% to 9.71%

- FY2014 8.25% to 8.97%

Cornerstone investors:

- Asian Century Quest

- Capital Research and Management

- Eastspring Investments (part of Prudential)

- Indus Capital

- Lion Global Investors

- Neuberger Berman

- Och Ziff

- Signature Global Advisors

- Quantum Partners (Soros)

The book building will close on May 15 and after the price is set, the public offer will start on 17 May and ends on 27 May. The pricing will give you a hint as to whether the demand for the stock is "strong". I am not sure if there are other special incentives given to the cornerstone investors but we shall see. In any case, i am not 'impressed' with this list of cornerstone. It has the smell of too many "hedge funds" and they are certainly not value investors.

Mr IPO's biased view

I have to tell you upfront that i am biased against the pay TV business in Taiwan. There is only one word to describe it - messy and cut throat. There are many players who want to get in the market only to realize how competitive and cut throat the business is and by being the No.3 player in Taiwan, i frankly don't see what so great about this business. If MIIF has been able to sell it, they would have sold it long time ago rather than "repackaging it" and selling to yield hungry investors now.

Financials

Let's look at the financials. Without reading the prospectus in detail, I am not sure how much the IPO proceeds will be used to "wipe out" the long term debt of the company which will then lower the interest and finance costs. I also don't understand why in taiwan, they have to pay such huge tax expenses which is even higher than the profit before tax. Again, i have not read the prospectus in details so i am just shooting off my cuff.

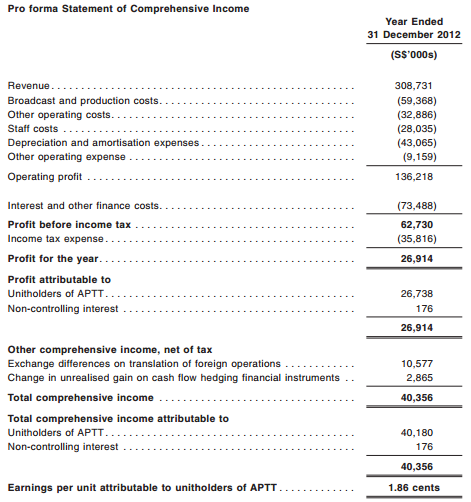

Proforma Statements

The pro-forma statements "looked somewhat different" as it has assumed the issuance of units to have taken place and in using the latest "In-thing" Chinese phrase “

停电魔术” the financials suddenly looked profitable and attractive.

Whatever it is, the majority of the proceeds will be used to pay off the original shareholder and not much will be used to pay down the debt. In the addition, i think the large number of units in issue will probably "cap" the upside.

Let's see if my biased views will change in the coming weeks. I will not give you my ratings and fair value for now. Please check back this blog again when the IPO is officially launched. ^_^

Comments

Macquarie only invests 3% and new investors are in for 97%. I estimate Macquarie makes $60 million related to this deal from MIIF and MKOF bonus, fees, and new annual management, etc.

Macquarie asks for a fixed yearly fee but the work is done in Taiwan, not Singapore. These corner stoner investors are fooling themselves: APTT has to raise close an extra $300 million to pay contingent liabilities and only get back less than this as dividends in three years for which current MIIF investors will get diluted below current NAV. (Ok, 95% of NAV because of new deal negotiated by CIMB Bank for Macquarie.)

For IPO success, look at performance deficit in MIIF of about $600 million. So, who is smart now?

有線電視分級付費 降價有望

【聯合報╱記者彭慧明/台北報導】 2013.04.25 03:44 am

有線電視收費降價有望!國家通訊傳播委員會(NCC)昨天通過「因應數位匯流調整有線電視收費模式規劃」草案,預定在民國一○六年推動分級付費制,屆時民眾可選擇收費兩百元以下的「基本普及組」,另自由搭配系統業者提供的頻道套餐組合,頻道套餐總費用以五百元為限。

NCC規畫在五月上旬針對本項草案舉行說明會,八月新制上路,但先不採行分級收費制,而是根據系統業者「數位化」程度,也就是類比頻道與訂戶裝設數位機上盒的數量,做為每年檢討收費的依據,數位化進度未達標或落後的業者,將被迫降價。

NCC說,目前有線電視採單一固定費率,上限為六百元,NCC已訂定一○六年為有線電視分級收費的「日出年」,屆時將全面採用分級付費,頻道套餐總費用上限為五百元,與現行的六百元比較,等於打了八三折。

據了解,行政院數位匯流方案明訂有線電視全面數位化時間表是「二○一四年」,即民國一○三年,NCC訂定一○六年為有線電視分級收費的「日出年」,似乎暗示全面數位化進程將延後。

根據NCC草案規畫,一○五年底,縣市政府在審查下一年有線電視費率時,將要求系統業者提出基本頻道分級收費方案包括一組費率上限為兩百元的基本普及組,三組(或更多)的套餐組;單一套餐組收費上限暫定一百元或一百卅元。用戶可以訂購基本組加上套餐組,但總費用不得超過五百元。

NCC說,系統業者提供的基本組加上前三組的頻道套餐,數量不可低於現在類比系統提供的頻道數,業者可增加套餐選擇,所有套餐加總收費以五百元為限,如為個別頻道則不受五百元限制。

[[ anonymous 7 ]]

Can you explain what “停电魔术” means?

What magic is this, and what does the phrase really mean ?

[[ anonymous 7 ]]

Thank you for answer.

I've a further question once the hullabaloo about stagging this Taiwan Pay-TV IPO is over.

As of the announcements yesterday pursuant to the divestment advocated by the Board of MIIF, MIIF shareholders will own 36.60% of APTT, whose only asset is TBC. [525.866 million MIIF APTT Units / 1,436.800 million Total APTT Units.]

That is right. MIIF shareholders have received the right to own less of the TBC asset via the APTT IPO. Naturally, this raises many questions.

But first one obvious observation: had MIIF shareholders kept the asset, it would seem the proposed dividend yield to MIIF would have been higher, and thereby the price of MIIF higher.

By the way, check the new propectus on page 53. (There are additional and amended disclosures post MAS review.) Without cash from the IPO (Unitholders' equity!), decreased capex and additional borrowings, the proposed distribution of $114.786 million would be more likely $72.215 million, a figure closer to the $69.019 million proposed dividend in 2013. (Oh yes, this $69.019 million itself includes "excess cash" of US$19.1 million which had not been distributed to MIIF and MKOF shareholders.)

So, how does the math look now? I have a much different yield than what is brazenly on the first page of the prospectus. You may too*.

I suggest you show these comments to your finance and law professors and ask them what they think.

The law professors may explain that disclosures are made to protect the party disclosing. (MAS just makes sure all the key disclosures are there.) The finance professors may explain that it is question of valuation and deconstructing the cash flow statement. You can hold both of them accountable by saying it is an indictment of the marketplace and asymmetry of information.

If you want something to look at, look at the 20 February, 2013 MIIF Circular for roles of various parties, e.g., CIMB, Macquarie, the Board of Directors, etc.

And as a student of law, perhaps I may direct you to this statement from the prospectus:

"Certain legal matters in connection with the Offering will be passed upon for the Trustee-Manager and the Sponsor as to Singapore law by Allen & Gledhill LLP and as to U.S. federal securities law by Clifford Chance Pte. Ltd., and for the Joint Bookrunners and Joint Underwriters as to Singapore law by WongPartnership LLP and as to U.S. federal securities law by Latham & Watkins LLP.

None of Allen & Gledhill LLP, Clifford Chance Pte. Ltd., WongPartnership LLP and Latham & Watkins LLP makes, or purports to make, any statement in this document and none of them is aware of any statement in this document that purports to be based on a statement made by it and it makes no representation, express or implied, regarding, and takes no responsibility for, any statement in or omission from this document."

Anyway, hopes this helps.

I see you are not a holder of MIIF and I expect you will not be a holder of APTT. Please tell us more about "underwater."

[[ anonymous 7 ]]

re : Without (a) cash from the IPO (Unitholders' equity!), (b) decreased capex and (c) additional borrowings, the proposed distribution of $114.786 million would be more likely $72.215

==========================

To put more simply, I think the questions raised are :

a. are unit-holders cash being recycled to pay unit-holders a dividend?

c. are borrowings being used to pay unit-holders a dividend? << this is known as a "dividend re-cap".

b. (no comment on point (b) above).

Dividend re-caps are quite common in LBO (Leveraged Buy-Outs) and PE (Private Equity) situations.

This PE dividend-recaps have made quite recent and large re-appearance in European PE situations, rising a lot of questions.

PE is looking for a chance to exit, and apparently some difficulties are being experienced. Amtek [M1P.SI] is a good example of a LBO / MBO refloation. From memory, Amtek [M1P.SI] involved StanChart and KKR.

Anyway, keep having a look at all these PE stuff, and get familiar with it?

I don't think this is a question of material mis-statement as a matter of having a close look at all the details buried in the prospectus.

Having some knowledge of the modus operandi of PE is useful. Points (a), (b), (c) are most salient from a financial perspective, and the business prospects (see the comment in chinese above - 4 May 2013 11:16) are also relevant.

The amtek deal was done by stanchart and Cvc Asia. The courts Asia deal also involved getting debt and paying out dividends. Done by barings Asia. Not that this is wrong, just the modus operandi to boost IRR to equity investors.

All new IPO shareholders go in with eyes open big big please...

These are prepared in advance of the lodgement of the IPO with MAS from talking points, models and seminars given to the underwriters' analysts by the Company and its lead bankers, which is this case would be Macquaie, et al.

Get a hold of one or two of these and you and/or good buy side analyst friend should be able to unravel the deal for you. Just don't leave it in tatters.