Elite Commercial REIT ("Elite" or the "REIT") is the first UK-focused REIT to be listed on SGX with more than 99% of the properties being leased to the UK government.

Elite is offering 114,686,200 Units for subscription at 68 pence per unit (or $1.21) of which, 5,734,300 units will be available for public subscription. In addition, 77,827,900 units were allotted to Cornerstone investors.

The IPO will close on 4 Feb 2020 at 12pm and commence trading on 6 Feb 2020 at 2pm.

Portfolio

The portfolio comprises 97 quality commercial buildings located across the UK and is primarily occupied by the Department for Work and Pensions ("DWP") - the largest public service department responsible for crucial welfare, pensions and child maintenance services for ~20 million claimants.

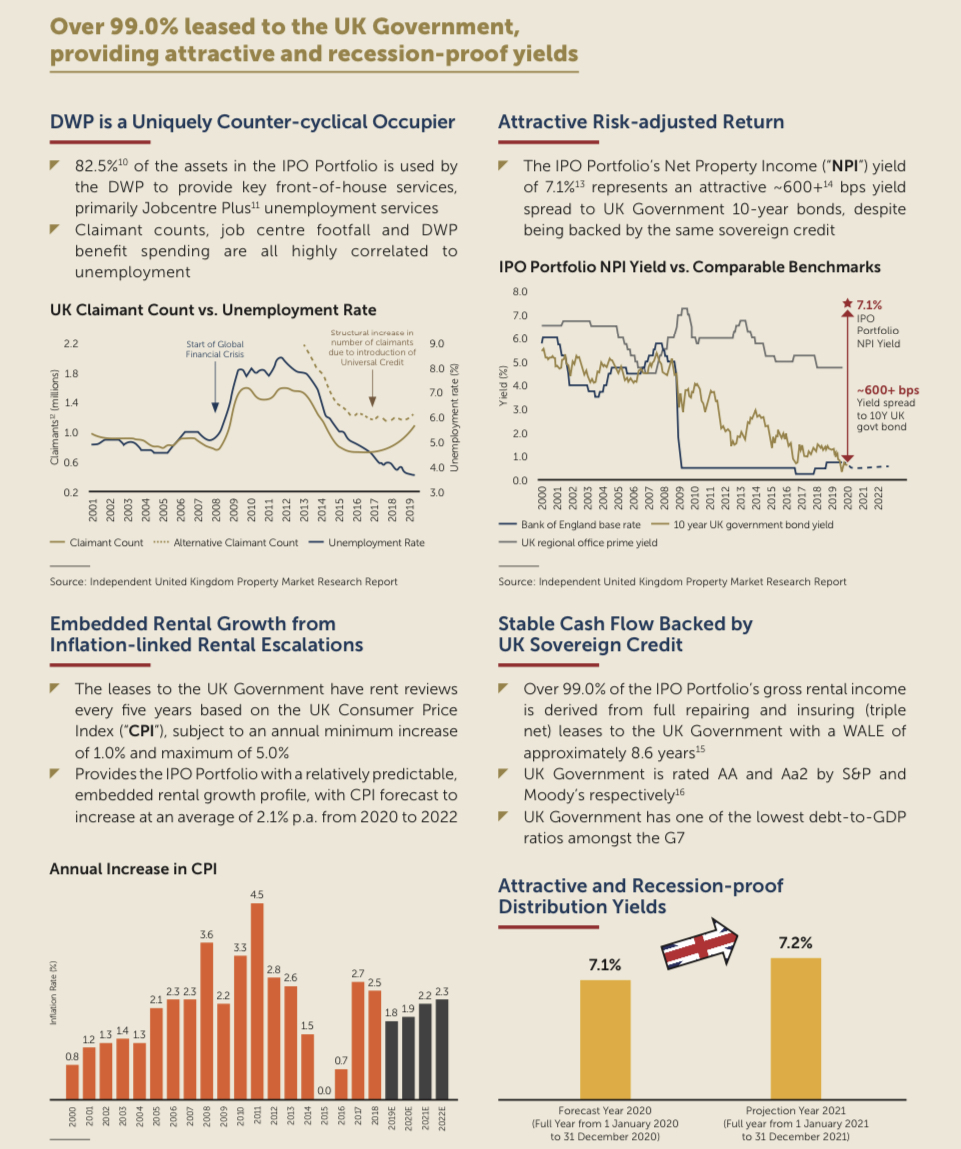

There are 96 freehold properties (and 1 property with lease till 19 May 2255) across United Kingdom with a 100% occupancy rate. The weighted average lease expiry ("WALE") is 8.6 years.

Distribution

The first distribution period will be from listing date to 30 June 2020 and will be paid on or before 30 Sep 2020. The distributions will be declared in GBP and unless investors elect to receive in GBP, it will be converted to SGD at the exchange rate at that point in time. The distributions will not be subject to further tax in Singapore.

The second distribution will be in Q1 2021 (within 90 days of close).

Financial Forecast

The forecasts above used a lower forex rate of GBP 1 : SGD 1.76. In this regard, if you are "bullish" on brexit and positive on the movement of GBPSGD rate, then your yield will be higher than 7.1%

You can see the foreign exchange rate sensitivity analysis on page 124 of the prospectus.

What I like about the REIT

- Over 99% leased to the UK Government - meaning there is a very low likelihood of "bad debt". As shown in the chart below, the yield of 7.1% represents a spread of ~6% to UK government bonds (rated AA by S&P and Aa2 by Moody's)

- Embedded rental growth from inflation linked rental escalation - The leases are reviewed every 5 years based on UK CPI subject to annual minimum increase of 1% and maximum of 5%

- Freehold properties and long WALE of 8.6 years - the properties are freehold and the long WALE provides certainty and stability of income

- Social benefits once given out, is hard to take away - the properties are used to provide crucial social benefits, which in my view, is tough for any government to "remove"

- REITs are currently the "flavor" of 2020 and the leverage of 33.6% is manageable - REITs have been performing well until the coronavirus hit the market last week. The leverage is not too aggressive

- Right of first refusal for 62 commercial properties located in UK that are on long term leases to the UK government

Some of my concerns

- Single country risk - Investors must be comfortable that they are taking on both the sovereign (government) and geographical risk of United Kingdom. Having said that, the properties are well diversified across different regions across UK

- GBP risk - with the brexit out of the way, it actually provides more clarity and certainty for investors. Investors are now taking on GBP/SGD risk and GBP is at 52 week high against SGD. Any depreciation of GBP will lower the yield to investors

- No major shareholders or Sponsor - The biggest shareholder is Ho Lee Group Trust at 10.8% (assuming over-allotment is exercised), followed by Sunway RE Capital at 8.2% and Kim Seng Holdings at 6.9%. The top 3 effectively controls 25.9% of the REIT, while the Sponsors only hold 19% on a combined basis. I would prefer a stronger alignment of interest

- Cornerstone investors are primarily HNWIs - the issuance are widely distributed to the wealth banking clients of UBS, BOS and CIMB and they hold 23.4% of the enlarged share capital and are not subject to any lock-ups. The HNWIs are offered leverage to take up this IPO

- Assets are not "grade A" offices - while the buildings are leased to "AA-rated" government entities, it doesn't mean there is a ready use for the building should the lease be extended. The value will probably "drop" if the government no longer wants to lease them or decide to relocate

- Artificial "yield" due to payment of management fees in units - had the units been paid in cash, the 7.1% yield would have dropped to 6.3% in FY2020

Fair value

At an yield of 7.1%, i thought the issuance is attractively valued but it was so difficult trying to find the price to book ratio. Why can't the issuer just state the figure out there. Is it intentional not to show the NAV per unit? Some bloggers computed and said the price to book is around 1.17x based on "historical" and 1.03x based on appraised values. No idea who is right or wrong but i certainly don’t like to be digging high and low on the figure in the prospectus.

Chilli Ratings

I will give this IPO a 1.5 chilli ratings.

Please note that this IPO is not for flipping but more for constructing a portfolio of REITs for income production.

I like the stable and sovereign credit backing the rental cashflows and the 7.1% yield, which is pretty decent in current market. The fact that the manager is electing to receive its fee in units also provide some assurance (if we think positively) that the longer term outlook is favorable. Otherwise, they would have elected to receive the fees in cash.

The size of the public tranche is pretty small at 5.7m units and the Wuhan coronavirus, Brexit uncertainty, GBP exposure, poor market sentiments and over-allotment to private banking clients may put off some investors.

You can decide if you want to apply at the IPO or buy it later post issuance. You should however, compare it against other listed REITs before deciding whether you would like to buy Elite Commercial REIT. Do note that post IPO, the trading of GBP denominated REIT is untested.

Happy IPOing

Comments