Hyphens Pharma International Limited

Hyphens Pharma International Limited ("Hyphens" or the "Company") is offering 29.6m shares at $0.26 each of which 3m will be for the public and the rest via placement. The IPO will close on 16 May 2018 at 12 pm and starts trading on 18 May 2018. The market cap based on the IPO price will be $78m.

Principal Business

According to the prospectus, Hyphens is one of the leading specialty pharmaceutical and consumer healthcare groups. The history dates back to 1998 and Hyphens has a direct presence in 5 ASEAN countries - Singapore, Vietnam, Malaysia, Indonesia and Philippines and distribution networks in Hong Kong, Myanmar, Brunei, Cambodia and Oman.

The group now comprises 3 core businesses:

- Specialty Pharma Principals - Exclusive distributorship to market and sell a range of specialty pharmaceutical products in the ASEAN region. Revenue from this segment accounted for 53.6% of total revenue for FY2017

- Medical Hypermart and Digital - Medical hypermart for healthcare professionals and online B2B platform. Revenue contribution for FY2017 is 35%

- Proprietary Brands - develop, market and sell own branded range of dermatological and health supplements such as Ceradan, TDF and Ocean Health (see picture below). Revenue contribution is 11.4% for FY2017

Key Competitive Strengths

Key Competitive Strengths

Financial Highlights

Financial Highlights

Looking at the revenue trend, i like the fact the revenue is increasing and has increased from $78m in FY2015 to $113m in FY2017. While the net margins has declined from 6.46% in FY2015 to 5.4% in FY2017, the EPS has improved from 2.1 cents to 2.5 cents correspondingly.

It is good to see the Company presenting the pre and post IPO EPS. Based on the post IPO 300m shares and the EPS of 2 cents, the historical price-to-earnings ratio is 13x. According to the prospectus, the NAV per share is around 10.8 cents.

The Company will pay at least 30% of its net profit as dividend. Assuming the EPS remains the same (conservative), 30% x 2 = 0.6 Singapore cents. That translate into a yield of 2.3%. This will be the "minimum yield" for FY2018 (hopefully).

Fair Value

Assuming the revenue continue to grow by 20% and net margin "dropped" further to 5%, net profit will be $6.79m and that will translate into EPS of Singapore 2.26 cents. That translate to a forward PE of 11.5x.

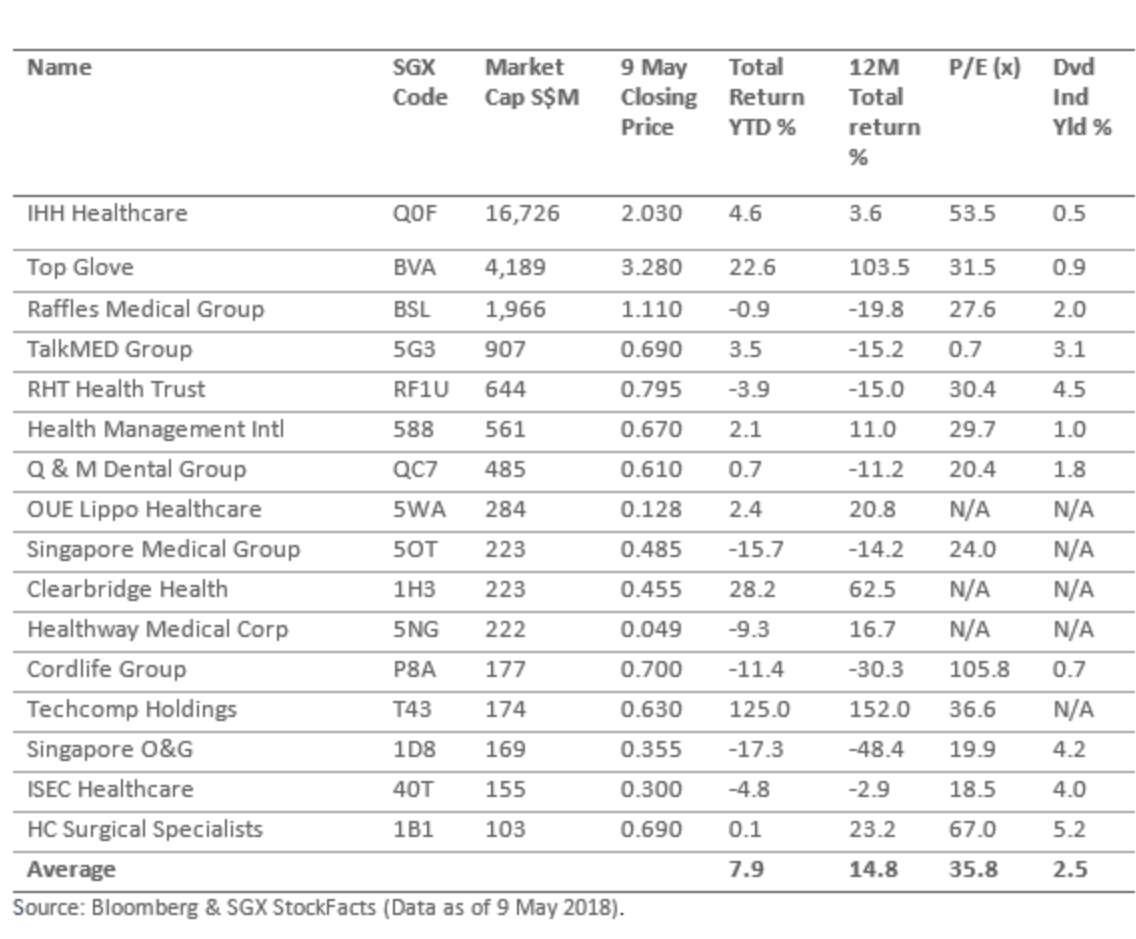

According to the recent SGX research report in May 2018, the healthcare stocks are trading at a "healthy" average PE of 35.8x and a dividend yield of 2.5%.

I will use a more conservative PE of 16-20x for my fair value computation. Based on the EPS of 2.26 Singapore cents, the

fair value range will be between 36 cents to 45 cents.

Use of proceeds

Ownership structure

Ownership structure

The public investors will only hold 9.9% of the Company with the Cornerstone investors holding the other 10.1%. Innomed Holdings (61.1% Mr. Lim See Wah and 38.9%) will hold about 65.4% of the Company with the balance held by Mr. Tan Chwee Koon. The shares will be very tightly held.

Future Plans

The Company intends to implement the following strategies:

- Expand and Strengthen its product range - launch 5 proprietary branded products in 2018 and expand its range of health supplements. It also intend to develop drug products for skin conditions and acquire product formulation for next generation line of Ceradan products

- Scale its presence in existing markets and expand to new geographies - expand marketing and distribution network by leveraging existing network and into new ASEAN countries, Australia and Middle East

- Enhance and leverage its online platform - to capture opportunities in the new digital age

- Expand through M&A, JVs or Alliances and improve operational efficiency by consolidating its operations into a new integrated facility and using automated packaging to increase production efficiency

What I like about the Company

- Strong ASEAN presence - I like the fact that the company has an established presnce in ASEAN. It makes the company attractive in two ways - acting as a distributor for established brands where the brand owner needs to work with just one company for scale. The other attractiveness will be that it will be more attractive to a potential acquirer. The Company would do well to continue scaling up and having a direct presence in the entire ASEAN region

- Regulated industry - Healthcare is a heavy regulated industry and this is a double edge sword, depending on which side of the fence the Company is in. It makes it difficult to crack into new businesses but once you are in, it is pretty monopolistic in that regard

- Proprietary brands - The proprietary brands will allow the company to brand its own products and enjoy better control over the costs and margins. The downside will be how it manages the relationships with other established brands to avoid potential conflicts

- Cornerstone investors - The IPO is supported by Nikko Asset Management, Qilin Asset Management (family office) and Maxi-Harvest Group. They will subscribe for 30.4m shares

- Attractive Valuation - The IPO is priced very attractive relative to its peers that are listed on the stock exchange. In fact, it is priced to debut well.

- Dividend paying - I like profitable and dividend paying companies. The Company intends to pay at least 30% of its net profits as dividends for FY 2018 and FY 2019 and that translate into a yield of more than 2.3%

Some of my concerns

- Expansion and execution risk - ASEAN is a diverse region with different regulations and cultures. It will not be as straight forward setting up presence and gaining market share. In addition, setting up of online platform will likely reduce the selling prices of products and that may not be well received by the brand owners. As such, the major risk will be the execution of its business plans

- Highly regulated and competitive industry means that there could be time delay or the products may not be successful registered or launched in the respective countries. The pricing of the products could also be controlled by law. In addition, the competition may be strong even though the market could be fragmented

- Auditor - with no disrespect for the existing auditor, I would have preferred a big 4 that has more resources and best practices

Mr IPO Ratings

This is a pretty straightforward IPO for me. It is a

3 chill ratings based on the relatively attractive valuation, dividend paying mindset and the fair value range of 36 cents to 45 cents. Readers may want to know that i have refreshed the definition of my chilli ratings recently where the ratings will reflect what i think the opening price will be. You can read it

here.)

I have received 20,000 shares from the Placement (I asked for much more than that ...) and will be applying for more shares through the ATM.

Happy Hyphening

Polling Time

Will you apply for the IPO shares? You can participate in the poll

here.

Comments

Thanks for the useful write up,

For the private placement, which provide you are using ?

I am a treasures client and they said not available, is it only for Vickers or private client?

Thanks!

I have been trying to bid for several IPOs. Most of the time i gotten none or very small allocation only. Greatly appreciated if anyone can advise on methods for a higher success rate..

what i mean is for example- apply 30,000 shares using my own OCBC acct and another 70,000 shares using my POSB acct. Is this consider illegal as well? Total transaction cost will be $2+$2. Was thinking of using this tactics for the next ipo. Cause my success rate has been on the extreme low side for ipo balloting.. =(