The Trendlines Group Ltd ("Trendlines" or the Company") is placing out 75.76m Placement Shares at 33 cents each for the IPO. It will be a pure placement tranche with no public shares and the market cap is around $168m. The IPO will close on 24 Nov and be listed on 26 Nov 2015.

What does Trendlines do?

Trendlines is basically an incubator based in Israel. It creates and develops medical and agricultural technological companies with a view towards a successful exit in the market place. The exits of these companies can either be a sale or IPO of these companies. The youtube video is

here if you are interested.

Investment Process

This is how the investment process of the Company looks like. Trendlines will invest up to $5m in a company with an expected exit horizon of 6 years or less.

I am not sure if you are familiar with the private equity market. There are many different "styles" or strategies, ranging from:

Seed (pre series) à Venture Capital (Series A and B) à Growth (Series B to D) à Pre-IPO à Buyout

The risk and reward profile is somewhat correlated with the different strategies, with seed having the highest risk but usually highest returns (if the investment thesis pans out).

Competitive Strengths

I will just "copy and paste" from the prospectus on its key strengths.

Interesting Cornerstone Investor

The IPO is supported by B.Braun, a private unlisted strategic investor based in Germany, to the tune of $7.1m or 21.515m shares. The website is

here. I am amazed that this Company was founded in 1839, employs 54,000 employees globally and generated sales of €5.43b but remains an unlisted company!

Portfolio Companies

The portfolio companies are in very interesting medical and agricultural technology space. These are currently very hot sectors to be in. Each portfolio company will be an interesting IPO candidate if it can be listed and can provide potential feedstock to our Catalist market here. Perhaps SGX is even more excited about bringing Trendlines to Singapore vis-à-vis other companies.

The list of top 10 portfolio companies are presented below with a nice vintage diversification ranging from 2008 to 2013. Some of these companies will be "ripe" for harvesting further down the road.

Track Record

In a nut shell, the Company is like an "investment holding company". In most cases, it is typically a listing of the "fund manager" except in Trendlines case, it is the fund manager plus the fund itself since it does not manage separate funds. This is a huge distinction which you need to make (which I will explain shortly). Anyway, the track record is presented below. It is interesting to note that it has sold companies to acquirers such as Baxter International and made ROIs of up to 67x.

What is the difference between a typical fund manager and Trendlines?

It is important to distinguish the different operating model between a fund manager and Trendlines. A typical fund manager manages funds and earns a management fee (2%) and carried interest (20% of cap gains) from the funds. These funds typically have an investment period of 3-5 years and a fund life of 10-12 years. Trendlines operates more like the "fund" and earns returns from the portfolio companies directly either through the dividends it receives or the capital gains when it sells the company, except in this case, the management fees is the "salaries paid" and it doesn't have a "fund life" per se.

Financial Highlights

The financial highlights are presented above. As highlighted above, earnings can be very lumpy due to different timing in realizing exits and potential write offs.

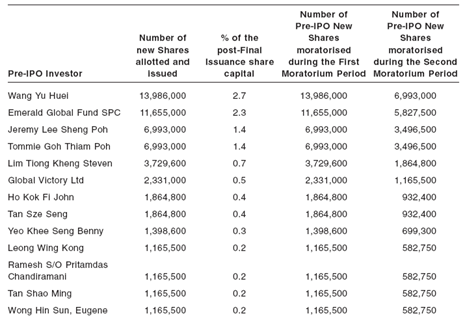

Pre-IPO investors

The pre-IPO investors consist of the usual players such as Alan Wang, Jeremy Lee and Tommy Goh. They bought in at around 21.45 cents but will be locked up for up till 12 months. I understand from the bookrunners that the IPO tranche was very well supported by the existing pre-IPO investors. In fact, almost all of them "doubled down" their stake by asking for more IPO shares and were cut back. It will be interesting to see if they can perform some local magic here…

What I like about the Company

- Israel is the 'hot bed' for technology companies and the Company is well positioned to incubate these companies

- I like the sectors in which Trendlines is focused in – healthcare and agricultural technology

- Strong management team and track record with Trendlines Medical being named "best incubator" twice

- Exporting its incubator business in Singapore and China. China should be a very exciting market if the Company can export its business model there

- Good cornerstone investor in B. Braun, a privately held global company with sales of more than €5.43b

- The IPO price is supported by the NTA of 24.39 cents (Price/NTA of 1.4x) with interesting pre-IPO investors

Some of my concerns

- The top 2 executives are very well remunerated and this may cause a drain on the cashflows, which are uncertain and depends heavily on the exit windows. The Company has been having negative cashflows since inception!

- Government funding on portfolio companies may stop in future

- Unpredictable income and profitability. It is very difficult to project earnings for this company due to its business nature and a lot is derived from fair value changes. You "can't eat" fair value appreciation

- It's not easy to fair value the investments

- Israeli government sponsorships may dry up one day or that the company may not win the mandates. This risk is probably low at this juncture

- Early stage investments carry a very high risk but also comes with high rewards

- Disperse shareholding structure with the top 2 executives owning less than 10% of the Company

Peers in Singapore

The peer I can think of is Hotung Investment Holdings Limited but the company is not "trading well" here currently with a 0.42x price to book. If Trendlines trade to that level, it will be below water

My Chilli ratings

Luckily there is no public tranche. Frankly I couldn't decide what chilli ratings i should give. On one hand, I like the sectors in which the Company is targeting. The list of pre-IPO investors and the cornerstone investor Braun, also help instill some confidence in the IPO. You may be able to see some first day "magic".

On the other hand, I am wary of the market sentiments as well as the poor peer performance of Hotung. I am also wary of the unpredictable profitability and negative cash flow since inception. Hopefully it will be at the infection point to be cash flow positive.

Based on the above reasons, I will give it a 1 Chili rating. Do note that I am vested...

Comments

So what is your guess on its price gain on Thu?

Thanks......