Memiontec Holdings Ltd ("Memiontec" or the "Company") is offering 33,485,000 Placement Shares at $0.225 each for a listing on Catalist. There is no public offering, as such, I am not going to spend too much time diving into the details. The offer will close on 3 March 2020 at 12pm. The market cap will be around $49.6 million.

Principal Business

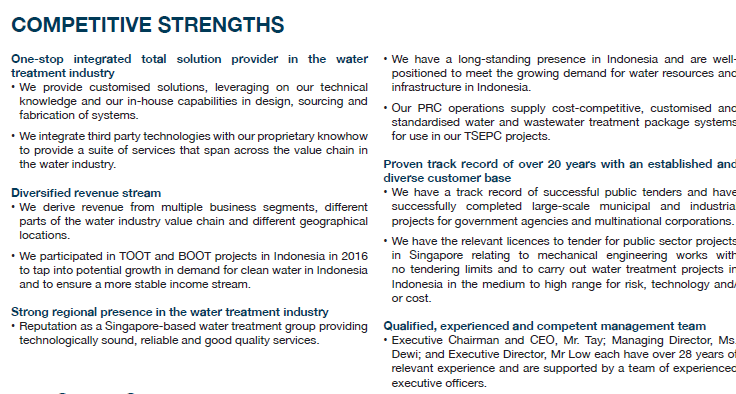

The Company is a one-stop integrated total solution provider in the water treatment industry with over 20 years of track record.

If you look at the description in the gatefold of the prospectus, they should really learn how to tell the story better. It is a mouth-full with all the TOOT and the BOOT acronyms. I almost wanted to say "toot" ... The Company could have made better use of the real estate in the gatefold to tell the story better and make it more concise, visually appealing and easy to read, sometimes, less is more.

Businesses include engineering and construction, operations and maintenance, sale of systems and equipment and the sale of water.

Competitive Strengths

Prospects

Financial Highlights

The post placement EPS for FY2018 is around 2.09 cents. Based on the IPO price of 22.5 cents, the PER is around 10.76x. Looking at 1H 2019, seemed like revenue has increased significantly to $14m but the profit fell to $355k. I am not privy to the forecasts but i would be concern if i am investing in this Company.

Dividend Policy

The Company intends to pay at least some of its profits as dividends for the next two years.

Shareholdings

The Company is tightly controlled by Mr. Tay and Ms Dewi.

What i like about the Company

I like the water sector as Indonesia is a big market with needs of clean water. It is like doing an ESG investment if this company can bring water to the community (perhaps the Company need to refocus on its branding angle). I also like the fact that company has a long track record with a dividend paying mindset.

Some of my concerns

Some of my concerns will be the forex exposure in Indonesia Rupiahs given some of its projects. In addition, the unpredictable income from EPC contracts as well as declining profitability would be something i need to further diligence on before committing.

Mr IPO Chilli Ratings

I am not going to spend much time on the chilli ratings as there is no public offering. As such, i have not shared my views on the company extensively as well. The Company has my sympathy as it could not have chosen a “worse” timing to list, with market sentiments badly hit by the market rout during the course of this week. The coronavirus is like a “black swan” event hitting all companies coming and no one could have predicted it coming. Having said that, given the small placement, share price movement may be well controlled but I would expect short term weaknesses as the pricing was done pre the market crash.

Good luck to those who were allotted the placement . . .

Comments