PropNex Limited ("PropNex" or the "Group") is offering 42.5m shares of which, 40.375m will be for placement and 2.125m for the public. There will be 12.9m new shares and 29.6m vendor shares. The offer price is $0.65 per share. Based on the IPO price, the market cap will be S$240.5m. The offer will close on 28 June at 12pm.

According to the prospectus, PropNex is the largest real estate agency in Singapore with 7,248 sales person and has a market share of more than 42% in both private and HDB resale market.

Business

The core business segments include real estate brokerage, training, property management and real estate consultancy.

The Group currently has presence in Singapore, Indonesia and Malaysia with plans to expand into Vietnam in 2018.

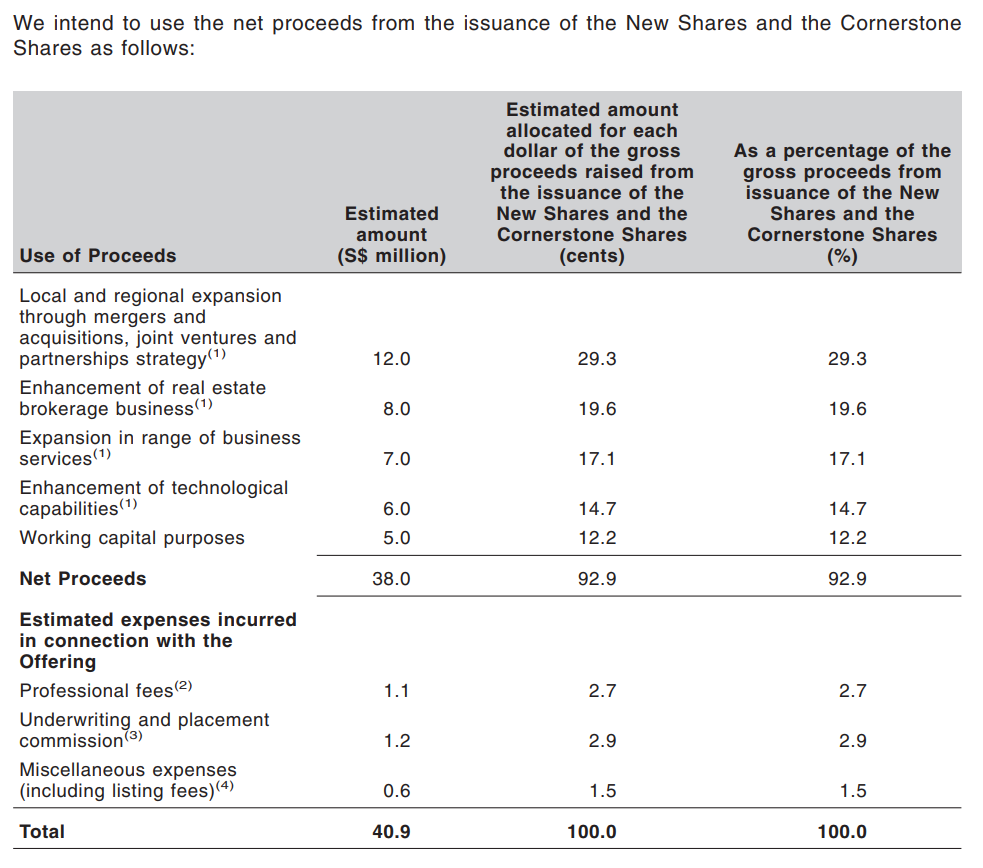

Use of Proceeds

The IPO proceeds net of expenses will be around $38m and the use of proceeds is as follows:

Financial Statements

I think there is a mistake here. The Group did not state the "Earnings Per Share" is in Singapore cents ? 🙄 It is still reflected under the S$ column. In any case, i will assume the Adjusted EPS is Singapore 4.4 cents

The Company has a blow out record year in FY2017 where the revenue was $361m and the profit for the year is around $18.9m. The adjusted EPS based on 370m shares is 4.4 Singapore cents. That translate into a PER of 14.77x

Dividend Policy

The Group intends to pay dividend that is at least 50% of its announced net profit after tax to shareholders for FY 2018 and FY 2019.

Assuming an unchanged EPS of 4.40 Singapore cents, a payout rate of 50% will imply a dividend of 2.2 cents. That will translate into a yield of 3.34%

Shareholders

The key shareholders are Mohamed Ismail, Alan Lim and Kelvin Fong. Collectively, they will own ~71% post listing with Mr. Mohd Ismail as the key shareholder. You can see that the shares will be tightly controlled post listing

What I like about the Group

- Presence of Cornerstone Investors - The presence of several reputable cornerstone investors will help provide some comfort on the IPO valuation. They comprise of known names such as FIL, NTUC Income, Affin Hwang, Samsung Asset, Value Partners and Nikko Asset Management. I would consider the cornerstone investors in PropNex to be better than the list in APAC Realty IPO

- Asset light and highly cashflow generative business - The agents generated the revenue which will then be paid out to them when the deal closes. There is low likelihood of "bad debts" as the sale proceeds are regulated and deducted directly from proceeds received by the seller

- Singapore property market is turning around - The local property market is turning the corner and if the volume can be sustained, the profitability of the Company can be assured

- Dividend paying stock - The Company intends to distribute no less than 50% of its net profit after tax to shareholders for FY2018 and FY2019

Some of my concerns

- Vendors are cashing out - The owners are cashing out and the vendors are P&N Holdings, Mr. Nizam Muddin Gafoor, Mr. Alan Lim and Mr. Kelvin Fong

- High dependency on Singapore's property market - The bulk of the revenue is derived from Singapore. Any market downturn in the Singapore property market will have a material impact on the Group

- Regulations - The local regulations are punitive to buyers of more than one properties and may introduce new measures if the property market becomes over-exuberant. On the flip side, if you hold the view that the government has already implemented all the punitive measures to penalise speculation, then the downside will be limited. Any lifting of curbing measures will be highly positive for the market

- Massive poaching ? It has happened in the insurance sector where teams crossed over to another competitor, but so far, this has not happened yet. In addition, the industry has undergone severe consolidation where the smaller agencies have now been merged or "subdued" under the bigger agencies

- Brokerage business is low margin business - The brokerage services while constitute 95% of the gross profit has a gross profit margin of 8.9%. There is little room for error if there are disruptions due to a "killer app" by other fintech companies (maybe Propertyguru?)

- Weak sentiments - The current market is not conducive for IPO. Even the red hot APAC realty has already cooled down and is trading at more attractive valuations than PropNex's IPO valuation

Peers Valuation

The main listed comparison will be APAC Realty that owns the ERA franchise. My previous write up is

here.

According to Capital IQ, APAC realty is expected to generate revenue of $451m in FY 2018 with a net profit of $30m and EPS of $0.08. It is trading at a PER of 10.48x. You can also assess the latest report by DBS Vickers

here. According to the report, current valuation is attractive for APAC Realty at 9.5x forward PE.

The share price has moved up significantly before undergoing the current correction.

In this regard, APAC Realty at 9.5x PER seemed to offer a better value proposition than PropNex Limited. As such, PropNex valuation of 14.8x seemed a tad too rich. Investors might as well buy into APAC Realty if they want an exposure to the Singapore market.

My Chilli Ratings

I will give it a one chilli rating. Buy if you really want to.

Reasons for not participating in this IPO will be the small public tranche, weak IPO sentiments and relatively better valuation in APAC Realty for investors who are keen to seek exposure to the Singapore property market.

Polling Time

You can also take the poll

here.

Comments