iX Biopharm Ltd ("iX" or the "Company") is issuing 65.5m shares at $0.46 each. The public tranche is for 1m with the balance through placement.

I will just do a high level "copy and paste" analysis on the Company. Before I start, I want to declare that I know nothing about this sector. You may want to refer to my post on

QT Vascular on how I "validated" the medical technology then.

Having said that and looking through the prospectus, this Company is probably too high risk for me and to be able to list under current bear market conditions at such high valuation is a really "astonishing" for me.

The Company is a drug development company with 3 drugs under development. It has its roots in Australia.

Financial Highlights

As you can see, this is a loss making company and its products are too early to generate substantial revenue. With a total equity of only $11.9m versus its listing market cap of $271.5m. Frankly, I don't know how to reconcile the two numbers. It's beyond my ability...

Perhaps the existing patents are worth something but it is definitely not reflected in the Company's balance sheet. The NAV per share is around 7.12 cents versus the IPO price of 46 cents. This is likely to pay for the "WaferiX Drug Delivery Platform" but i don't know how to prescribe a value to it.

The Company runs a negative cash flow business so investors will really need to take a long term bet on this business that the drugs will develop to its full potential.

Prospects

While it is interesting to have such listing, the Company is like a start up company to me. Its products are too early stage, pre FDA and with no firm timeline of meaningful revenue for the next few years.

For the products it is researching on, I am really ignorant about the competitive landscape. However, to develop a product on male erectile dysfunction when the blue pills Viagra is widely popular and easily available is beyond me unless the Company intends to develop a cheaper version to help clean out the illegal drug peddlers selling fake sex drugs in Geylang. ^_^

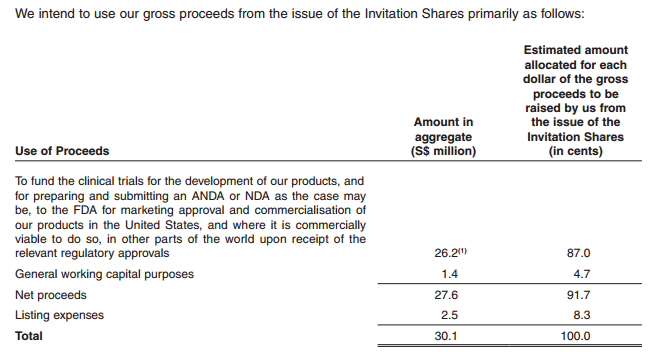

Use of Proceeds

As you can see from the prospectus, the Company intend to use the IPO proceeds is to fund clinical trials for the product development and for submission to the FDA (or its equivalent) for market approval and commercialization. As you can tell, IPO investors are bearing the development risks.

Management team remuneration

CEO Eddy Lee cam on board in Jan 2008. He has the biggest stake at 33.4% but it is amazing that he is not even medically trained and he was more involved in running casinos and the last casino he ran was Burswood in Perth. He sure has placed his chips correctly as his 33.4% stake is now worth $90.7m!

The management team other than him, is probably more experienced in this line but I don't like the fact that while the Company is bleeding, he has been getting a fat salary and been issuing shares to attract his team of management like Albert Ho and Philip Choo.

Shareholders

As you can see, Mr. Eddy Lee is the CEO with the biggest stake at 28.9% post IPO. Unlike the case of QT Vascular, i couldn't find other expert investors who can help validate the technology for me at IPO.

As you can see from the above table, public investors are paying 46c while earlier investors got in at between 6.7c to 12.5c. Of key concern to me is that there is a huge chunk of "other shareholders" at 39.9% post IPO. I don't like the way they do the disclosure as it is all lumped up in small print.

16.4% of the investors in this "others" category will not be subject to moratorium and i believe they have made good capital gains at the IPO price and will be most keen to get out if the price and volume is there. Once the moratorium is over, i am sure there will be renewed selling as well.

Mr IPO's views

While i like the healthcare sector and the fact that it is offering some shares for the public, I don't like this IPO for the following reasons:

- It is too early stage and IPO investors are taking on development risks

- It is priced at a very high valuation

- There are too many pre-IPO investors who got in a a lower price and some are not under moratorium

- The CEO is paying himself too much for this loss making company

- The current market sentiments is too weak for post market support

As such, this will be a zero Chilli rating for me and i will give it a miss (even though my good broker from CIMB offered me some shares - thanks!)

Happy IPOing

Comments

https://clinicaltrials.gov/ct2/show/study/NCT02356965